More AI models

Read more

AI bubble breakdown: which AI startups pop first and when

The "are we in an AI bubble?" debate is getting louder, but VentureBeat argues that's the wrong framing. The more useful question for you is which part of the AI market you're exposed to, and what the likely timing looks like. The article breaks the AI ecosystem into three layers with different risk profiles: wrapper apps, foundation model makers, and infrastructure providers. That's not just theory. It changes how you budget, how you evaluate vendors, and what kind of automation bets are safe to make in 2026.

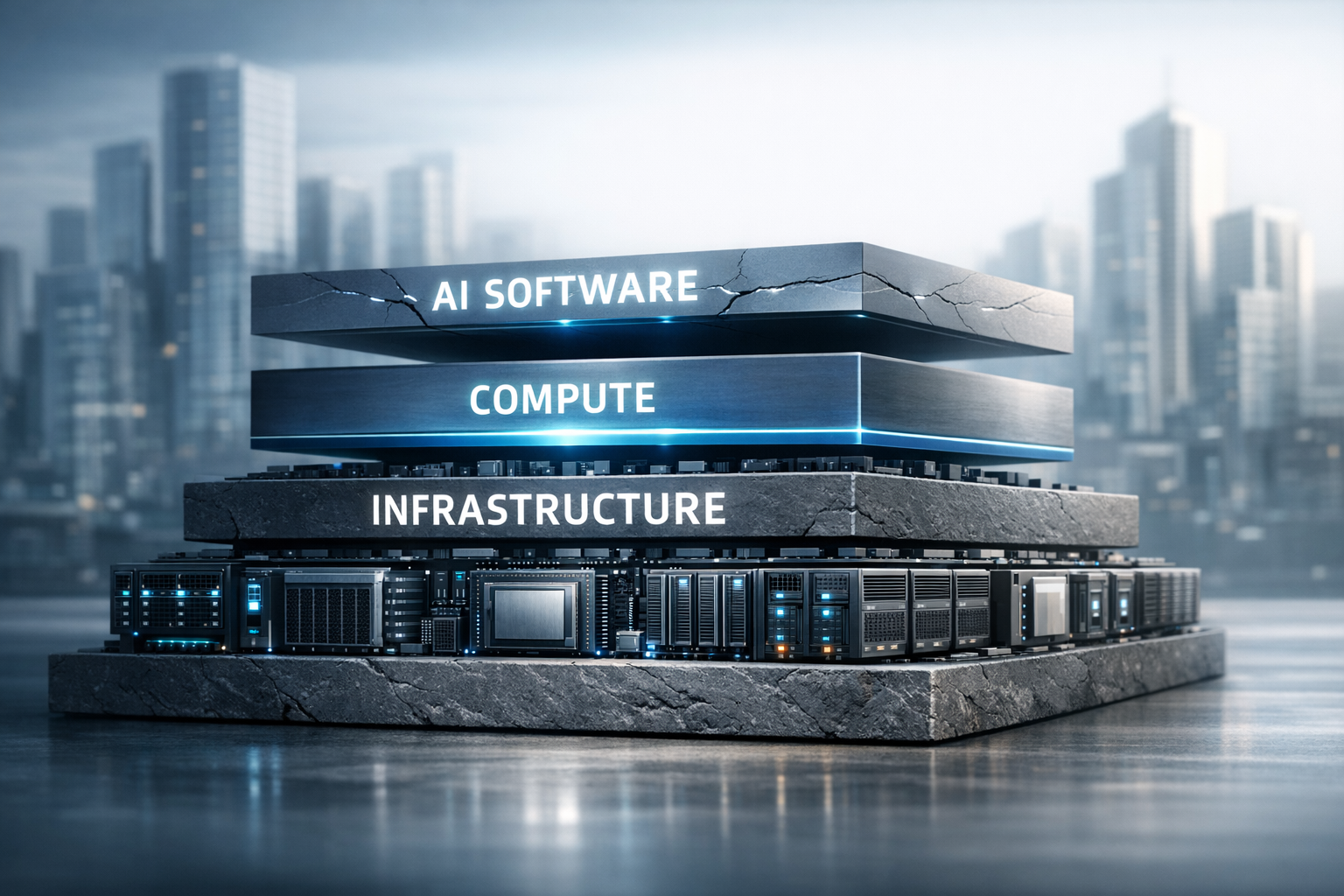

The article's core idea is that "AI" isn't one unified market that rises and falls together. It's a stack. Each layer has different economics and different ways to defend itself from competitors.

Layer 3: wrapper companies are the most fragile. They're often built by taking an API (like OpenAI's), adding a nicer interface and prompts, then charging something like $49/month for an app that isn't meaningfully differentiated from the underlying model.

Layer 2: foundation model companies (the teams building the large language models themselves) have more defensibility, but they also face big questions about spending, margins, and whether model performance becomes increasingly similar across competitors.

Layer 1: infrastructure (chips, data centers, memory systems, storage) is positioned as the most durable. Spending may fluctuate, but the physical capacity can still be useful as AI workloads grow over time, even if some businesses fail.

The timelines the article lays out are specific: wrapper failures are expected to show up first, late 2025 through 2026. Model consolidation comes later, 2026 to 2028. Infrastructure may see short-term volatility from overbuilding, but the long-term value is expected to hold up better.

If you've been pitched an "AI tool" that looks like a thin layer on top of ChatGPT-style outputs, this part is for you. The article says wrapper companies get squeezed from three sides.

The article mentions Jasper.ai as an example of fast early traction, reaching roughly $42 million in annual recurring revenue in its first year. That's impressive, but it doesn't automatically translate into durable advantage if the product can be replicated or bundled.

Business impact for you: if you're a buyer, wrappers can still be useful, but you should treat them like short-term productivity boosts, not long-term strategic pillars. If you're a builder, the warning is sharper: if your company is "just" a UI on top of someone else's model, your competitive horizon may be measured in quarters, not years.

The article names Cursor as a notable exception because it created defensibility through deep workflow integration and user stickiness. The point isn't that exceptions don't exist. It's that most wrappers don't do the hard work of becoming part of a real workflow.

The middle layer is where the industry narrative gets confusing, because it can be both true that (a) AI will be transformative and (b) plenty of companies will still fail. The article points to concerns around heavy spending relative to revenue at model companies like OpenAI, while also emphasizing that the best teams may retain real advantages.

Instead of "who has the smartest model" being the only game, the article argues that engineering execution becomes the divider as model capabilities converge. That means gains may come from things like inference efficiency, better systems design, and operating infrastructure in a way that's cost-effective. In other words, it becomes less about demos and more about the behind-the-scenes mechanics that keep AI affordable at scale.

The article also flags the possibility of circular dynamics in investment and demand, citing an example where Nvidia funds data centers that then buy Nvidia chips. The bigger takeaway for you is that supply chains and partnerships can amplify momentum - and also magnify a correction if assumptions change.

Still, foundation model companies have what wrappers often lack: deep capital, real technical moats, and strategic partnerships. The article's expectation is not an immediate wipeout, but consolidation from 2026 to 2028, leaving two to three dominant model players.

The article's contrarian claim is that the least speculative layer may be the one that sounds the most extreme on paper: infrastructure buildout. Chips, data centers, and AI-optimized storage are expensive, but the argument is that they can retain usefulness even if many applications don't survive.

It compares this to how earlier tech buildouts created capacity that later became essential. For you, the practical translation is straightforward: even if some AI startups disappear, there will likely still be ongoing demand for compute, storage, and high-performance systems as AI workloads expand and new use cases appear.

The article also says Nvidia's data center revenue reflects actual demand rather than purely speculative indicators. It doesn't claim the infrastructure layer is immune to volatility. It suggests a different kind of risk: possible overbuilding in the short term, followed by normalization, not a total implosion.

This is where the "multiple bubbles" framework becomes useful for non-technical operators. If your business wants the benefits of AI without getting caught in vendor churn, you need to separate automation outcomes from vendor hype.

1) Buy outcomes, not wrappers. If an AI tool is basically a repackaged interface on top of a foundation model, assume it could change pricing, features, or ownership quickly. That doesn't mean "don't use it." It means don't build fragile processes where a single wrapper is the only thing holding a workflow together.

2) Anchor your workflows in systems you already run. If you're already in HubSpot, ServiceTitan, or a CRM/ERP, focus your automation there. Use AI features and integrations that tie directly to your pipeline, tickets, job notes, and follow-ups. The article's message to builders is "own workflows" - as a buyer, you should prioritize vendors that clearly do.

3) Design for switching. Low switching costs are dangerous for vendors, but they're a gift to you if you plan for it. Use automation platforms like Zapier or Make.com as a routing layer so you can swap an AI step (summarization, drafting, classification) without rebuilding everything.

4) Automate the boring middle, not the marquee demo. The wrappers that get absorbed are often doing visible, generic tasks. Your edge is using automation in the messy parts of your operation: routing leads, generating quote follow-ups, summarizing call notes into your CRM, and creating internal checklists after customer interactions. If an automation saves you 12-15 hours/week of admin work, it matters even if the AI vendor changes - as long as the workflow is designed to survive a swap.

5) Be realistic about "moats" if you're building. If you're creating an AI product, the article's warning is blunt: staying a wrapper is the trap. Your defensibility comes from proprietary data, deeper integrations, distribution, and becoming part of how work actually gets done.

If you're using AI tools today (or evaluating them), here's a practical plan aligned with the article's phased "cascade" view.

The goal isn't perfection. It's resilience. The article's timelines suggest wrapper turbulence could hit quickly, so you want the ability to adapt without disrupting your core operations.

The article predicts a staged unwind: wrappers feel the squeeze first as margins thin and platform suites absorb features, then foundation models enter a consolidation era, and infrastructure spending cools without losing all value. For you, that means the "AI revolution" can still be real while your vendor list changes dramatically.

So the smartest posture isn't panic or blind optimism. It's operational flexibility: build AI into your workflows in a way that survives tool churn, and prioritize providers that are embedded in your day-to-day systems instead of sitting on top of them.

Source: This analysis is based on the layered "multiple bubbles" framework described by VentureBeat.

Want to stay ahead of automation trends? StratusAI keeps your business on the cutting edge, with practical workflows that don't collapse when the market shifts. Learn more and see what a resilient automation stack could look like for you.